interest rates, foreign exchange rates, and other market

conditions. If a counterparty defaults on a transaction that

is "in the money" for Swapco, the potential for loss exists.

Thus, counterparty credit risk is a critical factor in assessing

capital levels. Swapco minimizes counterparty credit risk,

and potential capital usage, by limiting new transactions

to investment-grade counterparties rated 'BBB' or higher.

If a counterparty's credit rating subsequently deteriorates

below investment grade, exposures must be fully capitalized.

At Sept. 30, 1995, the company had $691.4 million of

customer receivables without regard to collateral posted to

or received from counterparties. Of this amount, nearly

93% was due from counterparties rated 'A' or higher

(see

Counterparty Credit Profile table below). Based on notional

amounts, exposure to counterparties rated 'A' or higher

was approximately 90%.

To mitigate the adverse impact from large counterparty

defaults, individual counterparties are subjected to concen-

tration tests. Large concentrations must be fully capitalized,

with increasing levels of coverage for lower rated counter-

parties. Exposures are calculated using either gross or net

conventions, depending on conservative interpretations of

the enforceability of netting provisions in each domicile.

Affiliate Exposures

Swapco could incur significant exposure to affiliates since

all transactions are offset with SBHC, and Swapco also

guarantees certain affiliate derivative transactions. To

minimize this risk, Swapco's exposure to SBHC is calcu-

lated on a daily basis and fully offset with eligible collat-

eral, including a market volatility cushion to offset a

potential increase in the affiliate exposure during an un-

matched termination period. Under the company's operat-

ing procedures, all collateral must be of the highest quality,

consistent with an 'AAA' rating. Swapco also fully capital-

izes any exposures on guaranteed affiliate transactions to

offset current and potential liabilities.

Market Risk Management

Swapco eliminates market risk through offsetting,

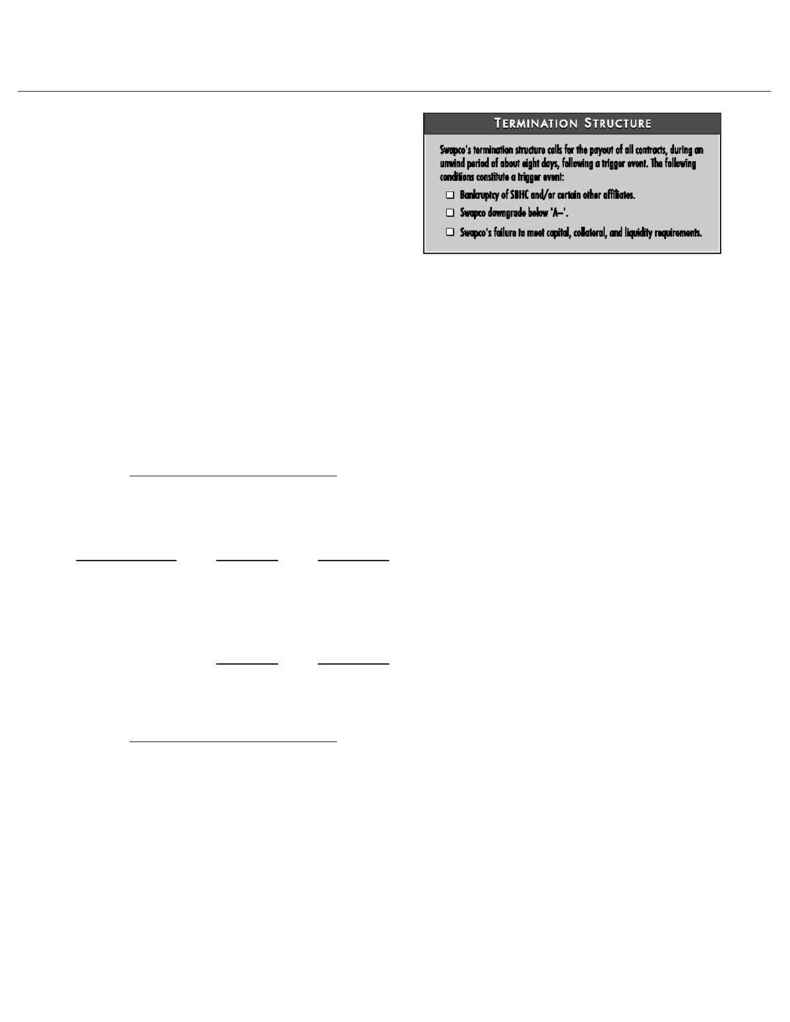

matched transactions with SBHC. Swapco's termination

structure calls for all transactions to be cash settled at

mid-market prices within eight days from a termination

event. Therefore, market risk is contained within a rela-

tively short termination period if Swapco's matched trans-

actions with SBHC cease to exist due to a trigger event.

Trigger events include SBHC bankruptcy; a downgrade of

Swapco below 'A'; or Swapco's inability to meet capital,

collateral, or liquidity requirements. Recently, Swapco

began providing each client with a quarterly summary of

the mark-to-market termination value of all trades using

mid-market prices.

To protect against adverse movements in the portfolio's

value during a termination period, SBHC posts sufficient

collateral to cover an adverse market change based on

historical measures of volatility. Swapco applies several

short-term, statistical measures of volatility and applies

the most stressful outcome to determine required collat-

eral. Fitch has compared the posted collateral cushion

against subsequent changes in the value of Swapco's

portfolio over the past two years. The results provide

confidence that Swapco's collateral cushion is sufficient

to protect against market movements during an eight-day

termination period.

Funding and Liquidity

Swapco maintains a high degree of liquidity through con-

servative investments in short-term, high-quality instru-

ments. At Sept. 30, 1995, Swapco maintained $109 million

of overnight repurchase agreements and cash. Swapco has

established a revolving credit facility with SBHC to meet

cash flow requirements from two-way collateral agree-

ments and other operating needs. The company has also

established a liquidity trigger to ensure that a minimum

level of liquidity is maintained through investments in cash

and cash equivalents. If Swapco fails this liquidity test, a

trigger event occurs. In a termination event, counterparty

Counterparty Credit Profile

($ Mil., As of Sept. 30, 1995)

Customer

Credit

Rating*

Receivables

Exposure (%)

AAA

324.8

47.0

AA

156.5

22.6

A

161.9

23.4

BBB

1.3

0.2

Other Acceptable

Counterparties

46.8

6.8

Total

691.4

100.0

*Long-term debt rating. Net exposure based on mark-to-market

valuations, excluding collateral received from or advanced to

counterparties. Note: Numbers may not add due to rounding.

Salomon Swapco Inc.

3

FITCH INVESTORS SERVICE, L.P.