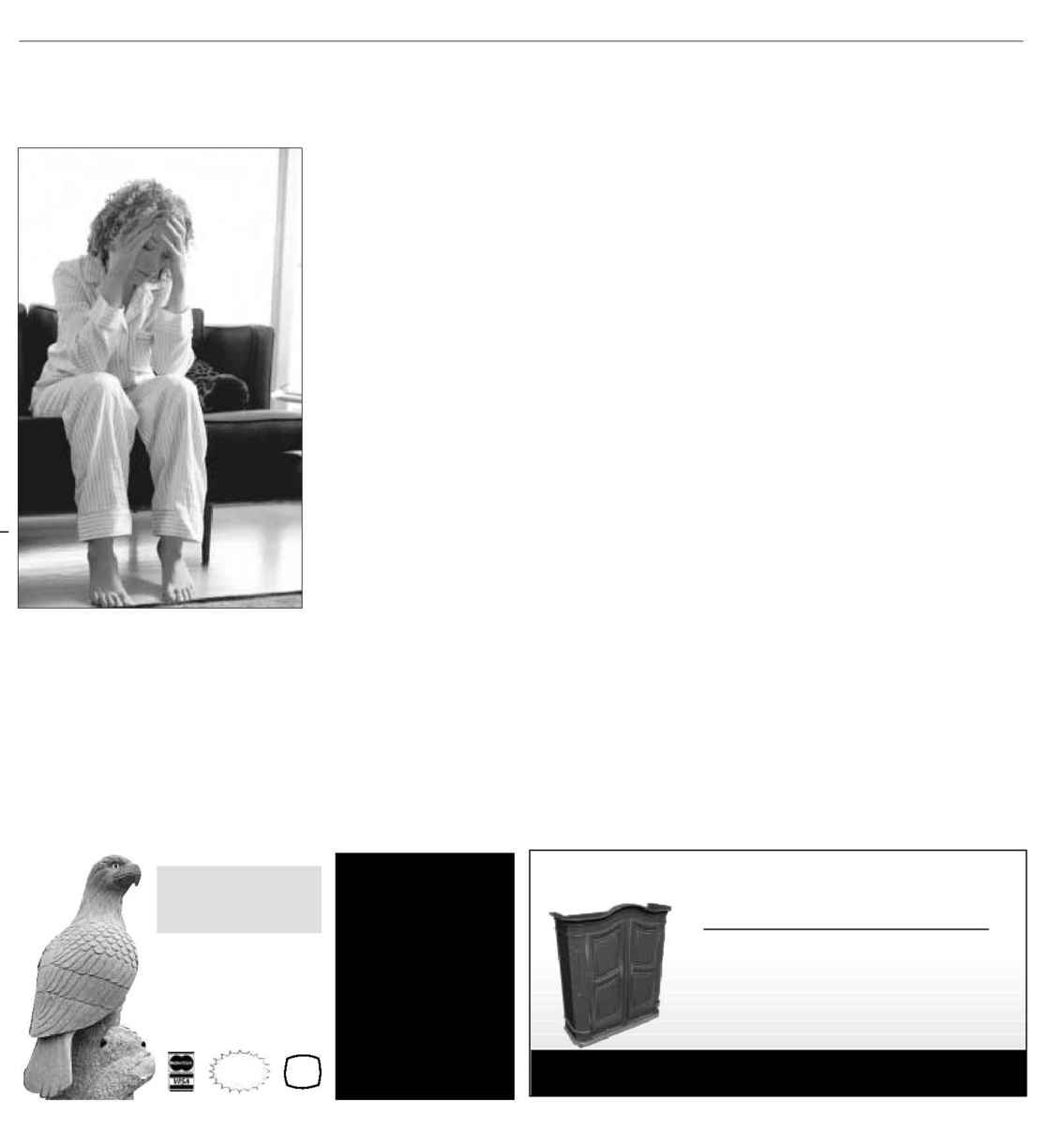

What keeps you awake at night? If

you're like most Americans, you've

probably more than once found your-

self up in the wee small hours, lying on

your back, staring at the ceiling above

your bed, having a little conversation

with yourself.

On the one hand, you're feeling

pretty good about things. But on the

other hand -- and this is why you're

awake -- there are those nagging little

questions that can get in the way of

anyone's peace of mind: "Am I doing

all that I should to protect my

current lifestyle? Have I done

enough to look after the people I

love the most? Am I doing

enough to take care of me?"

For many, the answer to these

late night eye-openers is a

resounding "no." That's because

those typical "everyday" con-

cerns such as paying bills tend to

distract people from thinking

about their long-terms plans. But

working with a financial profes-

sional can have a positive impact

on people, according to a recent

study commissioned by

Northwestern Mutual.

"We found that those people

who work with a professional

demonstrate more knowledge

about financial matters than

their counterparts who do not,"

says Janie Schiltz, vice president

of Northwestern Mutual.

"Moreover, the study reveals that

working with a professional can

have a positive effect on a person's

financial behavior as well."

Making a difference

A good advisor will immediately set

out to put your mind at ease when it

comes to helping you answer those

financial concerns that tend to keep us

all awake at night.

"There are a variety of ways to begin

this process of working with a profes-

sional," Schiltz says. "Some profession-

als will take a new client through a per-

sonal needs analysis -- a detailed ques-

tion-and-answer process that compares

a person's current financial approach to

their long-term goals regarding retire-

ment, education funding and similar

matters. The result of this process is

usually a report that provides the client

recommendations for accomplishing

his or her goals."

In addition to providing a thorough

analysis, there are a variety of other

ways that working with a financial pro-

fessional can make a difference.

For example, a professional can

show a client how to organize the

financial strategy into three buckets:

Those matters related to risk and pro-

tection, those regarding savings and

investing and those regarding retire-

ment and wealth distribution. A pro-

fessional can help a client grasp the dif-

ferences between term and permanent

life insurance and that owning the

right amount of life insurance is more

important than the type of insurance.

On the theoretical side, a financial

professional can help make a client

smarter by making him or her aware of

how "blind spots" -- like loss aversion

and mental accounting -- can affect

decisions in real-life financial situa-

tions.

"Blind spots are a product of emo-

tion and can handicap even the savvi-

est of clients," Schiltz says. "No one is

immune and when people become

aware of them they are much better

equipped to build a financially secure

future for themselves."

When you work with a professional

According to the Northwestern

Mutual study, those who work with an

advisor tend to have a more aggressive

investment mix, better savings habits

and more certainty about retirement,"

Schiltz points out.

For example, according to the

Northwestern Mutual study:

· Those with a financial advisor are

much less likely to be concerned about

the adequacy of their income or savings

in retirement, or about the future of

Social Security.

· When compared with those who

have no advisor, those with one are

more likely to have a target retirement

age and are more likely to anticipate

retiring at 64 or younger.

· Among younger people, those

with a financial advisor are more likely

to identify clear savings goals for retire-

ment than those with no advisor.

· Those with an advisor make larg-

er annual contributions (approximately

twice as much as those with no advisor)

toward reaching their financial goals

related to retirement, college educa-

tion, short-term needs and emergen-

cies.

Courtesy of ARA Content

No one likes to think about death or

make funeral arrangements when griev-

ing for a loved one who has just passed

on. Yet, when that dreadful day arrives,

someone has to do it, and decisions have

to be made quickly and often under great

emotional distress. And, like it or not,

death is a costly affair.

According to Funeralplan.com, a free

online consumer information and educa-

tional resource on funeral planning,

funerals rank among the most expensive

purchases many consumers will ever

make. A traditional funeral, including a

casket and vault, costs about $6,000,

although extras like flowers, obituary

notices, acknowledgment cards, or lim-

ousines can add thousands of dollars to

the bottom line. Many funerals run well

over $10,000. That's why many choose to

preplan and prepay their own funeral.

Preplanning allows you to compare

prices and services so that, ultimately, the

funeral reflects a wise and well-informed

purchasing decision, as well as a mean-

ingful one. When you prearrange, you

have control over the decisions relating

to your death -- the disposition of your

body, the funeral or memorial service and

what you want your obituary to say about

your life. You also relieve your family of

having to make important financial deci-

sions during a period of great stress and

grief -- a time when people aren't think-

ing very clearly and may not know what

to do because you never made your wish-

es known.

Preplanning your funeral can be as

formal or as informal as you want it to be.

It can be as simple as following a pre-

planning checklist and sharing your wish-

es with a family member, or it can be

made in the form of a preneed contract,

which can be set up with a funeral direc-

tor and prefunded through life insurance,

a bank trust agreement, or another

method. When done properly, preplan-

ning your funeral can give you peace of

mind.

Below are some guidelines to follow,

courtesy of Funeralplan.com, should you

decide to preplan and prepay your funer-

al.

1. Plan the actual funeral. Shop

around and talk to a few funeral directors.

Compare prices for such things as a cas-

ket, embalming and the cost for profes-

sional services. Resist one-stop shopping,

which can include such things as prayer

cards, thank-you notes and guest registers

-- they add up quickly. Many opt for a

funeral home in their neighborhood for

personalized services.

2. Decide on body disposition. Do you

want to be buried or cremated? If you

want an earth burial, a cemetery plot

needs to be purchased; if above- ground,

a mausoleum crypt. If cremation is your

choice, make a plan for how you will dis-

pose of the ashes. Do you want them

stored in a columbarium niche or buried?

Maybe you prefer to have your ashes scat-

tered. An option some people take is to

donate viable organs and tissues to a

medical school.

3. Decide on the type of ceremony.

You may want a traditional funeral serv-

ice with visitation and a member of the

clergy conducting services at a church or

a funeral home. Will you want an open or

closed casket? Maybe you want a special

friend to do the eulogy or family members

to read scripture passages or poetry. Any

favorite hymns? If you would rather have

a memorial service (a service in the

funeral home or a church where the body

is not present), express that wish. A com-

mon misconception is that when a body

is cremated, you don't hold a funeral. You

can hold a funeral before cremation if you

want to.

4. Tally the total cost of the funeral.

Tally all costs, which will probably be

considerable, and decide about prepaying

with bank savings, trusts, life insurance,

or annuities. Some of the costs involved

include:

· Basic services fee for the funeral

director and staff -- a fee that customers

cannot decline to pay that includes serv-

ices common to all funerals regardless of

the specific arrangement: funeral plan-

ning, securing the necessary permits and

copies of death certificates, preparing the

notices, sheltering the remains, and coor-

dinating the arrangements with the

cemetery, crematory or other third par-

ties. The fee does not include charges for

optional services or merchandise.

· Charges for other services and mer-

chandise -- costs for optional goods and

services such as transporting the remains;

embalming and other preparation; use of

the funeral home for the viewing, cere-

mony or memorial service; use of equip-

ment and staff for a graveside service; use

of a hearse or limousine; a casket, outer

burial container or alternate container;

and cremation or interment (the act of

placing a dead body in a grave).

· Cash advances -- fees charged by

the funeral home for goods and services it

buys from outside vendors on your behalf,

including flowers, obituary notices, pall-

bearers, officiating clergy, organists and

soloists. Some funeral providers charge

you their cost for the items they buy on

your behalf. Others add a service fee to

their cost, which they are required to dis-

close to you in writing, although they are

not required to specify the amount of

their markup. Funeral providers are

required to tell you if there are refunds,

discounts, or rebates from the supplier on

any cash advance item.

5. Draw up a will. Regardless of how

much or how little wealth you have, it's

important to have a will unless you want

the state to take over after you die. Have

a lawyer draw one up for you. Organize all

the papers and important documents

you'll need to take with you to the lawyer.

Your will is an inventory of all that you

own -- real estate, bank accounts, stocks

and bonds (if any), annuities and life

insurance. List your personal property,

such as jewelry, paintings, and col-

lectibles, and specify who gets what. Be

clear about the distribution of your assets,

but don't forget to list your liabilities --

mortgage, loans and credit cards. Sign

your will and have it witnessed by two

people with their correct addresses

included (should they be summoned by

the court). You will need to designate an

executor to administer your will after you

die. And, if drawn up by a lawyer, the

original copy will be filed at his or her

office. A duplicate copy should be kept in

a safe place where survivors will find it --

like a safe deposit box. (Remember:

Whatever is in your will is not set in

stone. You can make changes to it any

time you want.)

K

C

M

Y

The Citizen. Auburn, New York

Secure Your Future

Wednesday, January 31, 2007

9

4

Wednesday, January 31, 2007

Secure Your Future

The Citizen. Auburn, New York

How to preplan and pay for a funeral

Comprehensive Estate Planning.

Our planning services address not only estate tax

reduction, but also income tax reduction and asset

protection strategies.

Call today for a no-cost, no-obligation consultation, and start

charting the course for your financial future. 252-3600

DANIEL R. CUDDY

CPA, CFP

®

, CSA

*Advisory Representative

7 William Street, Auburn, NY

www.cuddyfinancial.com

252-3600

* Securities offered through H.D. Vest Investment Services

SM

, Member SIPC.

Advisory Services offered through H.D. Vest Advisory Services

SM

, Non-bank

subsidiaries of Wells Fargo & Company.

What Keeps You Awake At Night?

The Eagle

Has Landed!

Admire the workmanship

when you stop in to see what

we can do for your custom

memorial. Call today!

BARRE

GUILD

Veteran Owner - Jim Moulton

M

ID

-L

AKES

M

EMORIALS

(Justy Monuments ~

Gilboy Simpson Monuments)

253-7971

Open: Mon.-Fri. 8:15-3:15

Other times by appt.

131 Seymour St.

Auburn, NY

(Plenty Of Off-Street Parking)

10%

Veterans

Discount

Opening Early February

Winton Antiques

We Buy and Sell

·Estates ·Individual Items

·Coins ·Paintings · Militaria

·Estate Appraisals & Sales

117 Genesee Street

(Corner of State & Genesee)

Auburn,

Cell

# 729-3665 - Jerry Vevone